FiBAN deal flow is industry agnostic and we accept all applications from the New Nordic area. Of all applications roughly half get screened by FiBAN investors, 20% get invited to pitch, and 7% of applications raise interest from FiBAN angels and move forward into syndication conversations. The data is pretty much the same in comparison with the years scrutinized (2014-2021) for these results.

In addition, FiBAN investor members can bring and pitch their cases at the Pitch Finland event – which can be considered a “fast track” service for already validated cases.

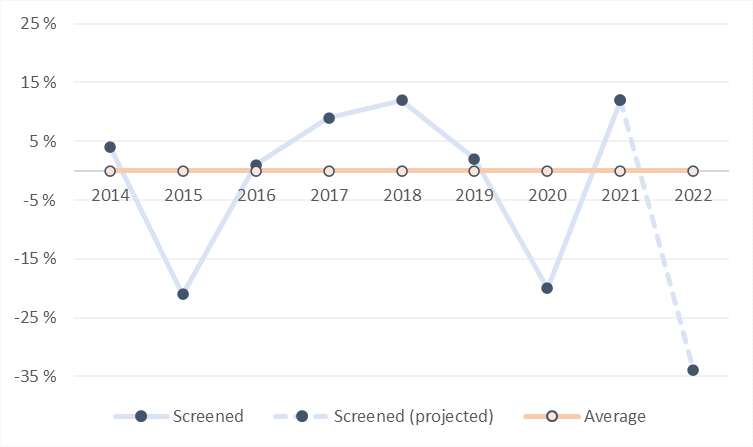

2021 peak in screened applications – reverse development in the share of applications that received funding

Here is a table that shows how the past 8 years can be compared to each other in terms of companies screened:

Table 1 shows a significant drop in screened applications during the pandemic year 2020 (-20% drop from the average), whereas 2021 marks one of the record-high years in the scrutin, with +12% increase compared to the average. Together with the remark on the decline of made investments in 2020, this might signal that the pandemic had investors focused on their portfolios instead of looking for new cases. Again the peak in screened applications in 2021 is in line with the latest annual angel investing data showing a record-breaking amount of investments made last year.

Looking at the future, we forecast a major decline in the deal flow for 2022. Of course, time will show how the deal flow develops in the H2.

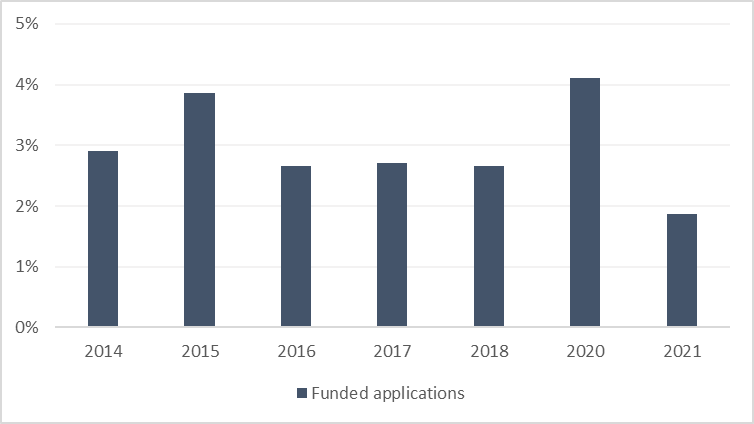

Looking at the share of applications that received funding (table 2), we see a reverse reaction compared to screened applications. Interestingly, the share of applications that received funding peeked in 2020 (4,1%). In contrast, in 2021, only 1,9% of applications closed funding, while 2021 still being a record year in startup funding in FiBAN history and in Finland in general.

From the data here we can conclude that FiBAN deal flow quality in 2020 was good. One explaining factor could be that as angel investors focused on their own portfolio companies, they directed deal flow to FiBAN. Meaning that more deals were shared from own portfolios thus opening the opportunity for other FiBAN investors to join companies with angels in, and suitable angel cases were directed more frequently towards FiBAN.

Three pillars for deal flow

If we think of FiBAN members’ deal flow and the reasons for joining FiBAN we can think of 3 different deal flow sources for a FiBAN investor:

One being the FiBAN deal flow; all the cases that come to the FiBAN deal room are visible to all our members and anyone can join the conversations. Second is the deal flow that they source themselves and leverage by increasing their own visibility in the networks as angel investors. And last but probably most efficient is the deal flow that business angels share with each other. The last point is something to cherish as well as it should be a common culture in general that would benefit everyone in the long run. Already in FiBAN ethical rules, we have 4 points out of 12 (points 4, 5, 6, and 7) that consider sharing and openness in deal flow.

Wishing everyone great deals, good deal flow, and remember to share those cases to make the deal flow flourish.

More information:

Antti Viitanen, Deal Flow Manager, FiBAN

antti.viitanen@fiban.org

Topi Laakso, Investment Analyst, FiBAN

topi.laakso@fiban.org